I remember the day, some few years back when I got a mail from my employer about submission of income tax-proofs. It got me into tizzy since that was the first time I had come under this process. A fresh graduate on landing a good job had never thought that goverment will play spoil-sport to him at the end of financial year.

With India shining, employement is rising and so is the entry level income. This is typically true of IT, ITeS industry where income level are sufficiently high for fresh graduates to seriously considering income-tax investments.

A first timer (I am only taking about service class first timers) should keep following things in mind:

1) Income tax calculation is NOT rocket science. A careful thought and study can easily unravel the mystry.

2) Do not make any un-informed decisions while saving for income-tax.

3) Usually employers deduct a portion of your income towards the tax every month. This is a good thing since this makes sure that you are not loaded with the entire income-tax at the end of year.

4) If your employer does not deduct any income-tax (which is extremely unlikely) then he is not showing you as a regular employee of the company on its payroll. Just confirm it.

5) Income tax rules change every year, so you should be aware of the latest rules for current financial year.

Some terminology which will be helpful for first timers:

Calender Year: January to December

Financial Year: April to March (currently income tax follows this cycle)

Income Tax: An amount of your income that goes to governement (what it does with that money is open to debate)

Tax Liability: The amount of tax you are liable to pay to government.

PAN : Permanent Account Number (PAN) is a ten-digit alphanumeric number, issued in the form of a laminated card, by the Income Tax Department. It is mandatory to quote PAN on return of income, all correspondence with any income tax authority.

Salaried Individual: You (this only includes your income)

Form-16: A form provided by your employer after all tax-calculation. This is the form that needs to be submitted to the goverment. It essentially tells what amoung of income you got and what amount of tax the employer cut and if there is any pending tax-liability.

Provident Fund: A fund set aside by government where an employer has to put certain portion of your income into it. Usually a same amount is put by employer on your behalf. So if 2000 INR is cut from your income and put into PF, then another 2000 INR is put by employer in your name into the PF. All the money in the fund belongs to you but only when you retire. So essentially government is making sure that even if act carelessely throughout your life without saving a single penny, you will have some amount of money in your PF account post retirement.If an employer makes you sign a declaration that you do not want a PF, do not sign it. Ask your employer that you need the PF.

Exemption: A tax-exemption implies that certain part of your income can be exempted based on certain criterion or if you spend your income on certain things (e.g. charity), you wont have to pay tax on the money you spent.

Deduction: If you put your money into some schemes or for some specific purposes, then you get a deduction

The main difference between 'exemption' and 'deduction' is that exemption is taken out before your gross taxable income is calculated, while deduction is reduce from gross taxable income to get the net taxable income.

Gross Taxable Income : This essentially is the amount you earned in this financial year.

Net Taxable Income: This essentially is the amount of your gross earnings that will be subjected to tax.

Income tax calculation is very easy, the confusion occurs because different people have different needs and different cases.

The indian income tax follows a progressive tax structure. The laws are made by Finance Ministry and modifications are made usually every year. The current tax-slabs are as follows:

Few important things to remmeber

Few important things to remmeber

a) There are various sections of Income Tax Act, few of which are important to know before you plan your income-tax saving.

b) The idea of providing income-tax deductions by the government is to increase the saving habits of an individual.

c) Investing for income-tax saving should not be confused with your other financial goals.

When you join a company, it usually asks you to fill "investment declaration". This is nothing but a declaration from you about how much investing/expenses you will be doing throughtout the financial year which can be accounted for tax-deductions or tax-exemptions. This declaration is just an estimate and has nothing to do with your final tax-investments. But it is usually best to be as close as possible to your actual investments. This is because all throughout the year your tax-deduction at source by the employer is done on this basis.

Around the timeframe of Dec-Jan, your employer will ask for actual proofs of investments for tax-calculation. This is the time-frame which is important, since in the coming Feb-March your income tax will be cut based on what proofs you submit. So if you fail to proivde any proof in this timeframe, your employer will cut taxes based on the fact that you have not done any investment (implying higher tax cut). In such a case, if you do invest in Feb-March, which is still in the current financial year, you will not benefit since the tax will already be cut. Although you will get your money back from IT department but that is a long-drawn process.

Then around March-June, your employer will give you a Form-16, which you need to submit to IT department. Once the Form-16 has reached you, your employer's responsiblity is over and now its time for you to submit it. If you loose it or are unable to submit, you will face penalty.

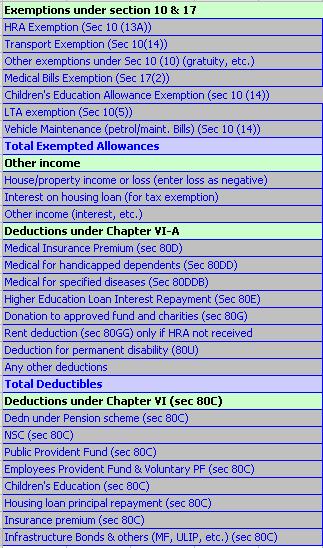

Some important sections under the current Income Tax Act for year April 2006- March2007 are as follows:

(Pic taken from the excel sheet by http://www.ynithya.com/taxcalc)

(Pic taken from the excel sheet by http://www.ynithya.com/taxcalc)

The most important for you would be :

a) HRA exemption: Your salary would have a component called HRA or House Rent Allowance. If you stay in a rented house, then you can avail this exemption. The formula is quite complicated

HRA Exemption = minimum of { 40% (50% in metro) of Basic+DA OR

HRA OR

rent paid - 10% of Basic +DA}

In most cities, the house owner refuses to give any receipt of the rent, then most people make fake receipts. Try to avoid such situations as far as possible.

b) Higher Education Loan Interest Payment Sec 80E : If you have taken education loan for higher studies, the EMI you pay consist of paying back prinicpal and interest. The amount of interest you paid in this financial year can be used as deduction under this section. Beware that just the interest repayment and not prinicpal repayment can be deducted.

c) Section 80C deduction : To increase saving from individuals, govt has decided to have a upper limit of 1 lakh INR investment under this section to be deducted from gross taxable income. Every scheme under this section (see list above) has pros and cons, so choose wisely. The following table will help you guide which investment has tax-benefit. The major change that has been introduced is that the interest/dividend generated from some schemes have become taxable making such schemes less attractive.

With India shining, employement is rising and so is the entry level income. This is typically true of IT, ITeS industry where income level are sufficiently high for fresh graduates to seriously considering income-tax investments.

A first timer (I am only taking about service class first timers) should keep following things in mind:

1) Income tax calculation is NOT rocket science. A careful thought and study can easily unravel the mystry.

2) Do not make any un-informed decisions while saving for income-tax.

3) Usually employers deduct a portion of your income towards the tax every month. This is a good thing since this makes sure that you are not loaded with the entire income-tax at the end of year.

4) If your employer does not deduct any income-tax (which is extremely unlikely) then he is not showing you as a regular employee of the company on its payroll. Just confirm it.

5) Income tax rules change every year, so you should be aware of the latest rules for current financial year.

Some terminology which will be helpful for first timers:

Calender Year: January to December

Financial Year: April to March (currently income tax follows this cycle)

Income Tax: An amount of your income that goes to governement (what it does with that money is open to debate)

Tax Liability: The amount of tax you are liable to pay to government.

PAN : Permanent Account Number (PAN) is a ten-digit alphanumeric number, issued in the form of a laminated card, by the Income Tax Department. It is mandatory to quote PAN on return of income, all correspondence with any income tax authority.

Salaried Individual: You (this only includes your income)

Form-16: A form provided by your employer after all tax-calculation. This is the form that needs to be submitted to the goverment. It essentially tells what amoung of income you got and what amount of tax the employer cut and if there is any pending tax-liability.

Provident Fund: A fund set aside by government where an employer has to put certain portion of your income into it. Usually a same amount is put by employer on your behalf. So if 2000 INR is cut from your income and put into PF, then another 2000 INR is put by employer in your name into the PF. All the money in the fund belongs to you but only when you retire. So essentially government is making sure that even if act carelessely throughout your life without saving a single penny, you will have some amount of money in your PF account post retirement.If an employer makes you sign a declaration that you do not want a PF, do not sign it. Ask your employer that you need the PF.

Exemption: A tax-exemption implies that certain part of your income can be exempted based on certain criterion or if you spend your income on certain things (e.g. charity), you wont have to pay tax on the money you spent.

Deduction: If you put your money into some schemes or for some specific purposes, then you get a deduction

The main difference between 'exemption' and 'deduction' is that exemption is taken out before your gross taxable income is calculated, while deduction is reduce from gross taxable income to get the net taxable income.

Gross Taxable Income : This essentially is the amount you earned in this financial year.

Net Taxable Income: This essentially is the amount of your gross earnings that will be subjected to tax.

Income tax calculation is very easy, the confusion occurs because different people have different needs and different cases.

The indian income tax follows a progressive tax structure. The laws are made by Finance Ministry and modifications are made usually every year. The current tax-slabs are as follows:

Few important things to remmeber

Few important things to remmebera) There are various sections of Income Tax Act, few of which are important to know before you plan your income-tax saving.

b) The idea of providing income-tax deductions by the government is to increase the saving habits of an individual.

c) Investing for income-tax saving should not be confused with your other financial goals.

When you join a company, it usually asks you to fill "investment declaration". This is nothing but a declaration from you about how much investing/expenses you will be doing throughtout the financial year which can be accounted for tax-deductions or tax-exemptions. This declaration is just an estimate and has nothing to do with your final tax-investments. But it is usually best to be as close as possible to your actual investments. This is because all throughout the year your tax-deduction at source by the employer is done on this basis.

Around the timeframe of Dec-Jan, your employer will ask for actual proofs of investments for tax-calculation. This is the time-frame which is important, since in the coming Feb-March your income tax will be cut based on what proofs you submit. So if you fail to proivde any proof in this timeframe, your employer will cut taxes based on the fact that you have not done any investment (implying higher tax cut). In such a case, if you do invest in Feb-March, which is still in the current financial year, you will not benefit since the tax will already be cut. Although you will get your money back from IT department but that is a long-drawn process.

Then around March-June, your employer will give you a Form-16, which you need to submit to IT department. Once the Form-16 has reached you, your employer's responsiblity is over and now its time for you to submit it. If you loose it or are unable to submit, you will face penalty.

Some important sections under the current Income Tax Act for year April 2006- March2007 are as follows:

(Pic taken from the excel sheet by http://www.ynithya.com/taxcalc)

(Pic taken from the excel sheet by http://www.ynithya.com/taxcalc)The most important for you would be :

a) HRA exemption: Your salary would have a component called HRA or House Rent Allowance. If you stay in a rented house, then you can avail this exemption. The formula is quite complicated

HRA Exemption = minimum of { 40% (50% in metro) of Basic+DA OR

HRA OR

rent paid - 10% of Basic +DA}

In most cities, the house owner refuses to give any receipt of the rent, then most people make fake receipts. Try to avoid such situations as far as possible.

b) Higher Education Loan Interest Payment Sec 80E : If you have taken education loan for higher studies, the EMI you pay consist of paying back prinicpal and interest. The amount of interest you paid in this financial year can be used as deduction under this section. Beware that just the interest repayment and not prinicpal repayment can be deducted.

c) Section 80C deduction : To increase saving from individuals, govt has decided to have a upper limit of 1 lakh INR investment under this section to be deducted from gross taxable income. Every scheme under this section (see list above) has pros and cons, so choose wisely. The following table will help you guide which investment has tax-benefit. The major change that has been introduced is that the interest/dividend generated from some schemes have become taxable making such schemes less attractive.

Thanks for the post. I was able to understand different components of IT which i finding difficult as a new joinee.

ReplyDeleteIts really helpful for all who are new.

ReplyDeleteThis comment has been removed by the author.

ReplyDelete