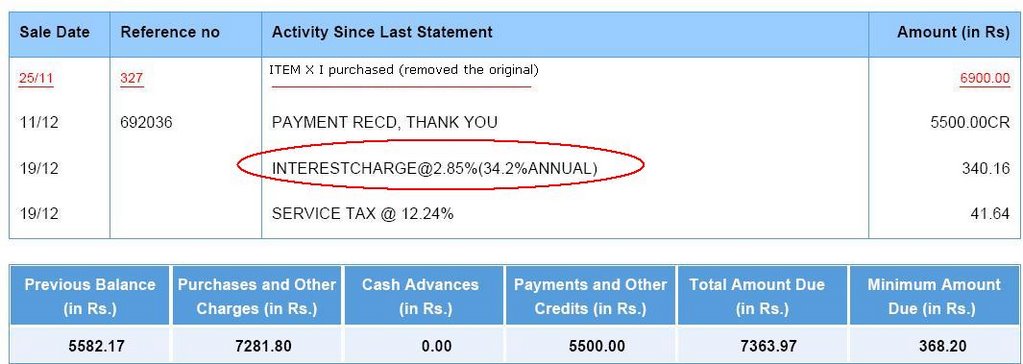

Now see the calculation of how the "interest" is calculate. I had outstanding balance of 5582 Rs in the previous month. Essentially this means I borrowed the 5582 Rs from citibank for one month. And on 25 Nov I again borrowed 6900 Rs for Item X. The due date of payement for 6900Rs is 14 Jan 07 and the due date for paying back Rs 5582 is 6th Dec. The cheque I issued against the previous due got cleared on 11 Dec, which means a delay of 5 days. So essentially they should charge interest for these 5 days.

With interest rate of 34.2% annually, the interest for 5 days should be 0.468%, but they have charged me interest for entire month (34.2/12 = 2.85%)... also they should charge interest only on Rs 5582 which should be Rs 159... but instead they charge intersest on the entire outstanding amount which is 2.85% of (5582 + 6900 Rs) = Rs 340 approx.

This is the way card companies make money. Imagine millions of customer paying such un-necessary amount. That is why credit card division is one of the most profitable business for any bank. This case is not exclusive to Citibank, but all card companies have more or less same terms. I have never shown much interest in knowing the terms and conditions, but now is the time I should look into it carefully.

Check out an interesting (although old, Nov 04) article by Robin Stein titled The Ascendancy of the Credit Card Industry.